The Commercial Real Estate Crisis is emerging as a significant concern for investors and financial experts alike, as skyrocketing office vacancy rates threaten to destabilize the economy. With major U.S. cities reporting vacancy levels between 12% and 23%, the impact on property values and local economies could be substantial. Kenneth Rogoff, a leading economist, warns that as commercial real estate loans approach maturity in 2025, financial institutions may face severe repercussions, potentially leading to bank failures if delinquencies spike. This liquidity risk, coupled with the Federal Reserve’s cautious stance on interest rates, has raised alarm bells across the financial landscape. The ripple effects of this crisis extend beyond just real estate, influencing consumer sentiment and lending practices in the broader economy.

This looming predicament in the commercial property sector, often referred to as the real estate downturn, is garnering attention for its potential to disrupt economic stability. With vacant office spaces dotting the skylines of America’s bustling cities, the ramifications on local businesses and overall market health could be profound. As experts like Kenneth Rogoff highlight, the significant debt associated with real estate assets maturing soon raises fears of a financial squeeze on lenders, which could trigger a broader economic slowdown. Understanding the ramifications of these high vacancy rates and the potential for rising delinquency rates among real estate loans is paramount for anticipating future shifts in the marketplace. The interplay of these factors not only threatens the financial stability of individual banks but could also reverberate through the entire economy.

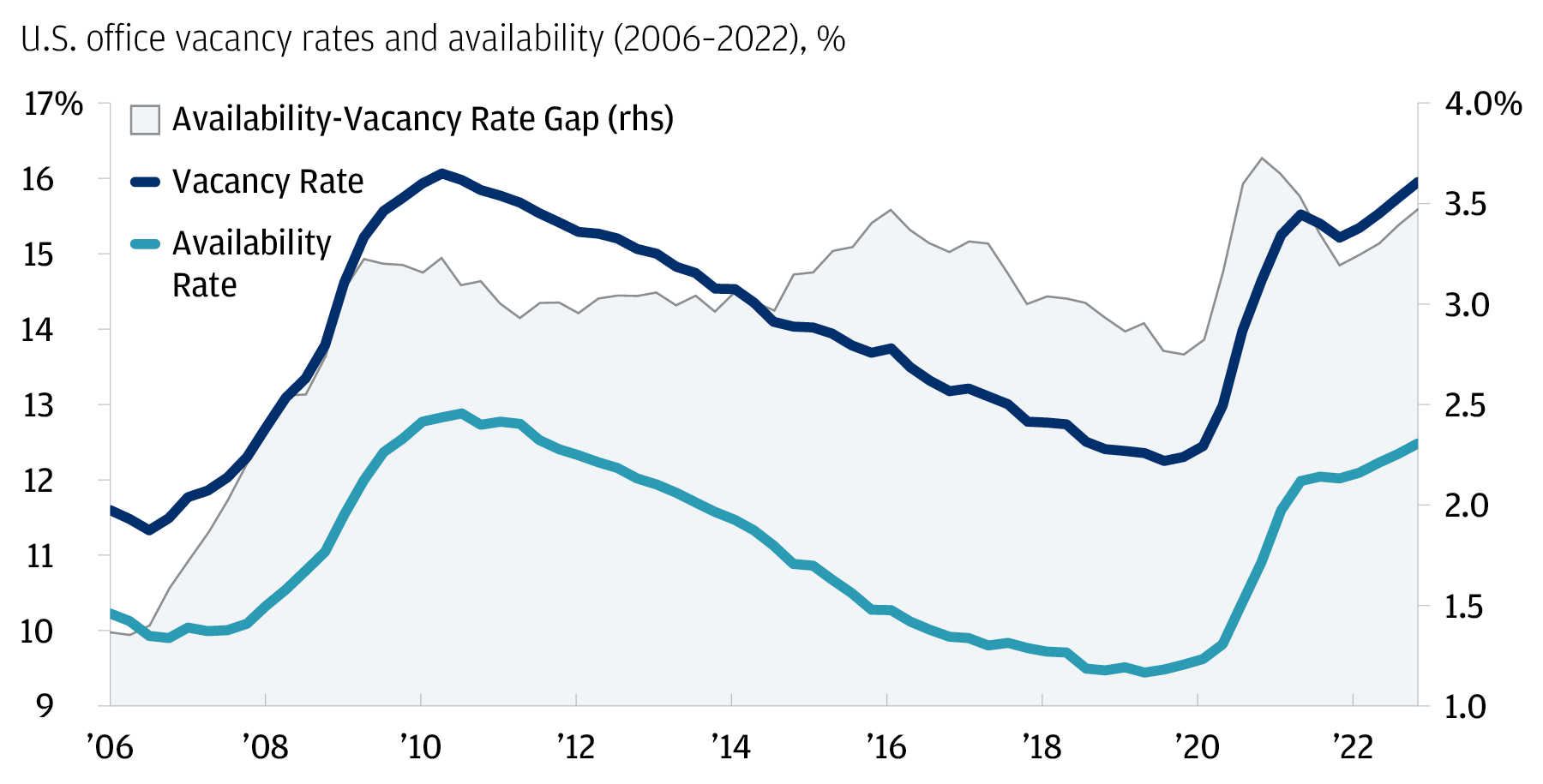

The Threat of High Office Vacancy Rates to the Economy

High office vacancy rates, particularly in urban centers, present a significant threat to the economy as businesses reassess their real estate needs in light of changing work environments post-pandemic. Currently, vacancy rates hovering between 12% to 23% result in decreased property values, putting pressure on owners and investors alike. This trend leads to a ripple effect of reduced tax revenues for municipalities and diminished economic activity in areas heavily reliant on business tenants. As companies continue to evaluate their real estate strategies, a prolonged stagnation in the office market could intensify financial strain, not just for landlords but for entire local economies.

Moreover, the extended high vacancy rates could exacerbate pressures on commercial real estate loans, as many properties struggle to generate the rental income necessary to service debts. With approximately 20% of the commercial mortgage debt set to mature this year, banks may face increased exposure to defaults if these properties do not quickly recover or find alternative uses. Simultaneously, reduced occupancy impacts ancillary services that thrive on office tenant bases, such as local coffee shops, cleaning services, and public transport, thereby intensifying the economic ramifications across broader sectors.

Kenneth Rogoff’s Outlook on the Real Estate Crisis

Economist Kenneth Rogoff provides a lens through which we can understand the escalating concerns surrounding the commercial real estate crisis. He suggests that while many firms within the commercial real estate sector will suffer significant losses—some properties potentially plunging in value by 50%—these challenges will not necessarily lead to a systemic financial crisis akin to 2008. With a solid outlook on the global economy amidst high interest rates, Rogoff emphasizes a critical distinction: the difficulties within commercial real estate may be severe but are likely manageable without engendering widespread panic among the larger banking institutions.

Rogoff highlights the importance of comparisons between today and past financial crises, noting that today’s larger banks have fortified their defenses through stricter regulations put in place following the last major meltdown. However, smaller banks with lesser oversight may feel the heat as they navigate the wave of maturing real estate loans. Rogoff’s nuanced view points out that while the impending losses will be painful, particularly for pension funds invested in real estate, the overall banking stability should withstand the storm if no other major economic shocks emerge.

The Lessons From Investment Behavior Pre-Pandemic

Prior to the pandemic, an era of near-zero interest rates fostered an environment where investors heavily leveraged their stakes in commercial real estate. This optimism bred a culture of over-borrowing, as many assumed that favorable rates would persist indefinitely. However, as interest rates climbed, this over-leverage left many with unsustainable debts, exacerbating the current crisis of high office vacancy rates. Real estate investors are now left grappling with the reality that their assumptions about perpetual low rates were misguided, leading to serious financial repercussions that are beginning to manifest.

Further complicating the scenario, the demand for office spaces has drastically diminished, with current occupancy in major U.S. cities providing a stark contrast to pre-pandemic levels. Many businesses have adopted strategies of remote or hybrid work, eroding the traditional reliance on physical office spaces. As the demand for office buildings continues to languish, the lingering question remains: how can unwanted commercial spaces be reimagined or repurposed? Despite innovative ideas surfacing, such as converting office buildings into housing, practical challenges such as zoning laws and structural hurdles impede swift resolutions for repurposing these financial burdens.

Potential Impacts of Bank Failures on Consumers

The specter of regional bank failures in the wake of commercial real estate challenges poses more than just risks to banks; it can significantly hamper consumer confidence and economic activity in impacted areas. Should a wave of defaults occur due to delinquencies in real estate loans, the resulting distress could restrict lending practices, leading individuals and small businesses toward tighter credit conditions. This tightening can ripple through communities, resulting in reduced spending and stalling economic growth, potentially leading to greater uncertainty across various sectors.

Furthermore, the relationship between banks and pension funds deepens the risks for the average consumer. With substantial investments tied to commercial real estate, losses may translate directly into diminished pension performance, gradually affecting retirees and future retirees alike. While it’s crucial to note that the broader economy may remain relatively buoyant, localized economic devastation in regions heavily invested in troubled real estate could lead to a divergence in economic experiences, creating pockets of financial hardship amidst an otherwise recovering market.

The Role of Interest Rates in the Real Estate Landscape

The current landscape of rising interest rates is a significant factor driving the commercial real estate crisis. As the Federal Reserve has hesitated to ease rates, the cost of borrowing remains elevated, affecting both consumers and businesses. For investors, the rising rates create hurdles in refinancing existing loans, complicating efforts to manage financial obligations against a backdrop of stagnant property values. The expectation of long-term high-interest rates not only hinders economic recovery in real estate but also heightens risks of a cascading effect across the financial system, as many firms find it increasingly difficult to secure favorable terms on loans or shift their financial structures.

This challenge underscores the urgent need for potential interventions aimed at stabilizing interest rates and revitalizing the flagging office space market. An anticipated decrease in rates could alleviate some of the financial stress, enabling investors to refinance existing loans and restore cash flows. However, experts like Kenneth Rogoff caution that such a scenario is unlikely unless a significant economic downturn occurs. Thus, the balance between maintaining rate increases to combat inflation and stimulating growth in commercial real estate represents a critical tightrope for policymakers and market participants.

Navigating Zoning and Engineering Challenges in Repurposing Real Estate

As the commercial real estate sector grapples with high vacancy rates, the prospect of repurposing office buildings into residential spaces presents numerous challenges, particularly in terms of zoning laws and engineering constraints. Many existing structures lack the fundamental design elements, such as natural light and proper ventilation, that are essential for livable residential environments. While the notion of transforming vacant offices into apartments may sound appealing, practical hurdles often derail these projects before they ever begin.

Additionally, zoning regulations can heavily restrict the changes required to adapt commercial spaces for residential use, leading to frustrating delays and heightened costs for developers. Heightened scrutiny from city planners and local communities often complicates these efforts, as concerns over neighborhood dynamics and existing infrastructure come into play. Addressing these challenges not only requires innovative architectural foresight but also collaborative discussions with housing advocates and local governments to create pathways for such developments, ultimately easing the burdens of high vacancy rates in the evolving landscape of commercial real estate.

Strategies to Mitigate the Commercial Real Estate Crisis

While the commercial real estate crisis poses significant challenges, several strategies can mitigate its impact on the economy. One potential avenue is for banks to explore alternative financing options tailored to properties struggling against high vacancy rates. By offering restructuring plans or longer loan maturities, lenders can provide relief to property owners who need time to stabilize their investments. Furthermore, fostering collaboration between private and public sectors can result in incentives that encourage the conversion of vacant office spaces into affordable housing units, addressing both economic and social issues concurrently.

Additionally, developing educational programs for investors about the risks of over-leveraging amidst changing economic conditions can help prevent further ill-fated investments. By focusing on sustainability and adaptability in commercial real estate practices, stakeholders can nurture a more resilient market capable of weathering future economic shifts. Ultimately, innovative solutions and concerted efforts can not only mitigate the current crisis but also position the sector for recovery, potentially leading to a revitalized urban landscape that caters to diverse needs.

Understanding the Long-Term Implications for Banks

The long-term implications of the ongoing commercial real estate crisis will likely shape the banking landscape in profound ways. As banks navigate increasing pressures from maturing loans tied to underperforming properties, a careful reassessment of risk management strategies will be essential. Enhanced compliance frameworks and an emphasis on diversified portfolios will allow banks to fortify themselves against future repercussions, effectively reducing exposure to volatile sectors. Additionally, the lessons learned from the current crisis may prompt larger institutions to invest more prudently in commercial real estate moving forward.

Moreover, regulatory bodies may respond to these unfolding events with renewed scrutiny aimed at smaller banks that have faced lighter oversight. Such changes could reshape the competitive dynamics in the banking sector, potentially leading to greater consolidation as weaker banks grapple with increased demands from regulators and the market. In this evolving context, maintaining a balance between fostering healthy competition among banks while ensuring systemic stability will be critical to avert potential pitfalls in the commercial real estate landscape.

The Future of Commercial Real Estate: A Cautious Perspective

Looking ahead, the future of the commercial real estate market remains uncertain but full of potential for transformation. The combination of lagging demand and a wave of maturing loans presents both challenges and opportunities for investors willing to adapt. While some investors opt to retreat from the commercial space, others may find opportunities in acquiring undervalued properties, particularly as valuations adjust to meet current market realities. Additionally, emphasis on sustainable and tech-integrated office developments could provide new avenues for growth and reinvigoration.

Yet, the path forward must be approached with caution as the complexities of the real estate market interplay with broader economic factors. High office vacancy rates may take time to stabilize, and proactive measures addressing structural overhauls, alongside responsive financial policies, will be crucial. Ultimately, fostering a collaborative ecosystem among investors, banks, and policymakers can pave the way toward a reimagined landscape that successfully balances economic viability with evolving workforce needs.

Frequently Asked Questions

How could high office vacancy rates contribute to the commercial real estate crisis?

High office vacancy rates, currently ranging from 12% to 23% in major U.S. cities, indicate a significant decline in demand for office space, which directly contributes to the commercial real estate crisis. This surplus of vacant properties leads to depressed property values, increasing financial distress for investors and lenders, ultimately impacting the broader economy.

What is Kenneth Rogoff’s perspective on the economic impact of the commercial real estate crisis?

Kenneth Rogoff warns that the commercial real estate crisis, driven by rising office vacancy rates and the expiration of real estate loans, could lead to significant losses for banks, especially smaller institutions. While he does not predict a widespread financial meltdown, he acknowledges potential regional distress and its ripple effects on the economy.

What might happen if numerous commercial real estate loans reach maturity without refinancing?

With approximately 20% of the $4.7 trillion in commercial mortgage debt maturing this year, failure to refinance these loans could result in widespread delinquencies. This may cause substantial losses for banks, particularly regional ones that are heavily invested in commercial real estate, and could exacerbate the ongoing commercial real estate crisis.

Are bank failures likely due to the commercial real estate crisis?

While some bank failures are possible, particularly among smaller, less regulated banks, Kenneth Rogoff suggests that a complete financial crisis akin to 2008 is unlikely. The large banks are better capitalized and diversified, potentially mitigating the impact of the commercial real estate crisis on the broader banking sector.

What role do rising interest rates play in the commercial real estate crisis?

Rising interest rates have made refinancing difficult for investors, many of whom over-leveraged during periods of low rates. These increased costs contribute to higher office vacancy rates and can lead to a surge in delinquencies on commercial real estate loans, compounding the current crisis.

How can the commercial real estate crisis affect consumers?

The commercial real estate crisis can negatively impact consumers by resulting in lower consumption in distressed regions and stricter lending terms. Although this sector struggles, a robust job market may offset some negative effects, making the overall economic impact less severe for the average consumer.

What trends indicate a future commercial real estate crisis on the horizon?

Key trends such as escalating office vacancy rates, the imminent maturity of large volumes of real estate loans, and the potential for economic downturns suggest a looming commercial real estate crisis. The intersection of these factors heightens concerns around financial stability and regional bank health.

Can the commercial real estate crisis be prevented?

Preventing the commercial real estate crisis might be possible if long-term interest rates drop dramatically, allowing for easier refinancing. However, many analysts expect that significant bankruptcies will likely occur in the adjustment process, making a complete prevention unlikely.

| Key Points |

|---|

| High vacancy rates in office buildings due to decreased demand post-pandemic, leading to property value declines. |

| A significant amount of commercial real estate loans, worth $4.7 trillion, is due by 2025, causing concern for potential bank failures. |

| Commercial mortgage debt constitutes around 20% of lenders’ assets, raising concerns about financial stability. |

| While losses in the commercial real estate sector are anticipated, a financial crisis similar to 2008-2009 is not expected. |

| The situation is exacerbated by over-leveraging and rising interest rates, decreasing remarkable demand for office spaces. |

| Smaller banks may suffer more than large institutions due to less capital requirement oversight. |

| Recovery in commercial real estate hinges on potential reductions in long-term interest rates. |

Summary

The Commercial Real Estate Crisis poses significant challenges for the economy today, primarily due to high office vacancy rates and impending loan maturities. As the landscape of commercial real estate continues to evolve, characterized by an oversupply of office space and high mortgage debts coming due, the implications for banks and investors are substantial. While the risks of widespread bank failures are present, the expected impact on the broader economy may be contained. Nonetheless, stakeholders must navigate these turbulent waters carefully, as shifts in interest rates and economic conditions could further complicate recovery efforts.